What happened with PayPal?

In this article I will share my journey with PayPal. What I learned. What I got wrong. And what remains to be seen.

At one point I was 100% allocated to $PYPL stock. This was prior to Q3 when things were looking a lot better for the company. Fortunately, I reassessed my position after seeing some things I did not like in December 2025.

The end result culminated in me realising a -10% portfolio value loss after selling the stock once Q4 earnings results were released and the shock news arrived sharing Alex Chriss had been replaced as CEO by the chairman of the board of directors.

A painful experience and a timely reminder of why valuation alone isn’t a thesis.

Let’s go back to the beginning

To understand how this disaster unfolded, it is helpful to go back to 2023. PayPal was in a death spiral trading in the $60s and infamous ex CEO Dan Schulman announced he was stepping down.

A young, talented, tech orientated rising star from Intuit named Alex Chriss was announced as his replacement. I saw a potential opportunity for a turnaround.

At the time, I believed PayPal still had a lot of potential due to its treasure trove of financial data, vast customer base and global scale as the most recognisable, trusted payment processor.

I entered the stock prior to Alex Chriss’s first earnings call as CEO. When listening to him talk about his plan for the future, I thought he sounded confident and ambitious. “We need to execute. And we will”.

He talked of monetising Venmo, the mistakes of legacy management and the potential for the future. I instantly took a liking to him and bought into his vision for the company.

He talked of transparency and honesty in results, which resonated with me greatly. Previous management were the opposite of transparent and he was acknowledging that.

The first few quarters were rough, as expected. The stock bounced around in the $60 range and progress was slow. Alex had his infamous interview on CNBC when he said “we will shock the world”, a phrase that would haunt him thereafter.

Six new innovations were announced:

A reimagined checkout experience

Fastlane By PayPal

Smart Receipts

PayPal Advanced Offers Platform

A Reinvented PayPal App (Cashpass)

Enhanced Venmo Business Profiles

The response was skeptical. The “we will shock the world” meme was born and it’s been a source of ridicule ever since.

Personally, I liked the plan. Reinvent the company, profitable growth.

“PayPal is a growth company” Alex said.

That phrase has aged very badly. But at the time it seemed plausible.

I didn’t care about the stock price. I was confident in the valuation and the potential for a turnaround.

I believed in the vision Alex was selling to me. And I deemed him to be the right man for the job.

Growth Slowdown

2024 highlighted problems with Braintree. The company decided to renegotiate all unprofitable contracts in an effort to stop Braintree from being a loss leader and competing with branded checkout.

This caused a slowdown in top line revenue growth which continued into 2025.

This drove the narrative that PayPal was a dying company which was impossible to fix.

I did not see it that way. I just thought it was going to take more time for the turnaround to materialise.

And that once Braintree was fixed, it would be adding to the bottom line as well as the top line.

With the benefit of hindsight, the warning signs were there which showed the turnaround was likely to take much longer than anticipated.

The market hates slowing growth. It doesn’t care about why growth is slowing. They are valued as a dying company. And it will punish a company until they can prove otherwise.

My Positioning

I ended up selling out between $90 and $80 in early 2025 in tranches when they projected this slowdown as I knew the market would punish them.

With an average of $61, this was a good move in hindsight.

I spent much of 2025 jumping in and out of the stock due to seeing more attractive opportunities ($NBIS at $20, $UNH at $240, $DLO at $10).

2025 was a good year for me, but to be brutally honest, it was not difficult to achieve good returns in 2025.

I also don’t put much weight into short term performance. It’s fairly meaningless.

I was looking for the best risk vs reward profile to park my money in the second half of 2025.

I started to believe $PYPL was an asymmetric opportunity due to its strong financial profile, buyback yield and cheap valuation.

Thought Process

On the approach to Q3 2025, I noted a few things which led me to believe a re-rating was imminent.

Free Cash Flow

FCF for the year was back loaded. The company was guiding for $6-7B in FCF. Yet they had only produced a total of around $1.5B for the first two quarters.

This was another metric the market was less than impressed with and rightly so.

Jamie Miller described FCF as lumpy, but guidance was maintained for $6-7B in FCF. Which to me was a signal that Q3 and Q4 should produce $2-3B in FCF per quarter.

Analysts were projecting much less FCF for the year than company guidance. A positive surprise for FCF two quarters in a row could destroy the narrative that $PYPL is dying. It could demonstrate its financial health and flip sentiment.

Or so I thought.

2026 guidance

Management stated on multiple occasions that 2026 was going to be an acceleration year in terms of top line revenue.

I was convinced 2025 was the last period of slowing growing growth before a major inflection point was reached.

With revenue acceleration combined with strong FCF, and increasing transaction margin dollars, I could see a situation where an aggressive re-rating took place based on these assumptions.

I still believe that re-rating would have materialised if they had replicated the momentum shown at Q3 earnings.

Alas, that was not the way it played out.

Sandbagging

PayPal had delivered mostly beat and raise quarters during my time invested with them.

I was confident in the execution.

Management said multiple times that if they guided for something, they had line of sight.

And they had not proved me wrong so far. Q3 came in as yet another beat and raise.

With guidance now raised twice during 2025, I viewed that as a signal that 2026 was going to be strong.

The bar was set low. So far this was working well and I had no reason to believe that was going to change anyone soon.

The stock price hadn’t been moving, but in my head, the business was firing on all cylinders. And that’s all that mattered to me.

Buybacks

The share count was now well under 1B. When the share count was revealed post Q3 as 935M, I started to view the buyback mechanics as a solid safety net.

Provided they kept increasing FCF and buying back shares, downside was capped. Or so I thought.

The lower the share price got, the more shares were repurchased and the more equity I now owned.

This, in combination with strengthening fundamentals is what gave me the confidence to go in heavy.

Limited downside, unlimited upside

That was genuinely how I was viewing the company at the time. Due to the mechanics of the buybacks, the increasing FCF and revenue growth, I could not see a realistic scenario where the stock was going below $60 outside of a market crash. My conviction was high, and remained so even after Q3, despite Jamie’s bearish commentary.

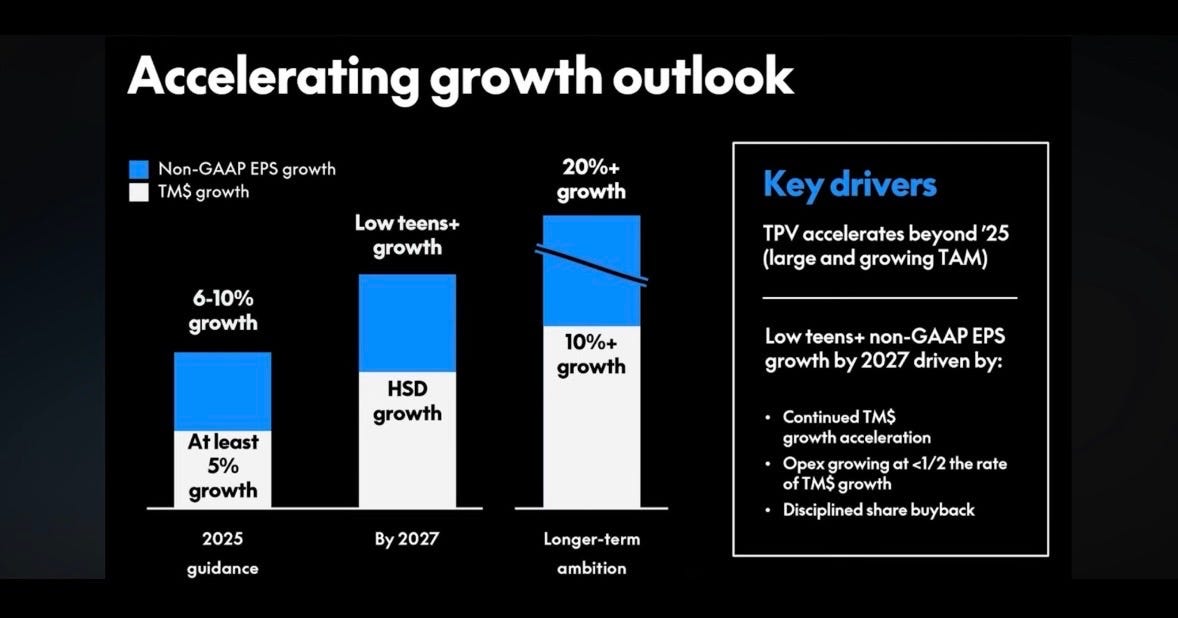

2027 guidance

In the not too distant future $PYPL was projecting ambitious metrics for the company.

This led me to believe that 2026 would be a strong year.

It would have to be if they were going to meet 2027 guidance. And seeing as management reaffirmed it multiple times since investor day 2025 and stated they would not guide for it if they did not see line of sight, I had no reason to doubt this roadmap.

What did I miss?

Hindsight is easy right?

Well I would not be so naive as to let myself off the hook that easily.

There were signs that appeared during the Q3 earnings call and continued thereafter. I called them out at the time publicly. So it’s not like I was blind.

Let’s break it down.

The Q3 earnings call

The company delivered a triple beat and raise for Q3, after announcing a partnership with OpenAI that morning.

The stock gapped up to $85 almost instantly, I was doing victory laps on X, thinking that PayPal’s hardest days were now behind them.

The first wallet to be integrated with ChatGPT. Earlier in the month, they announced an agentic commerce partnership with Google and a deepening of their existing relationship.

The ground was set for a generational run.

Alex Chriss sounded bullish. He talked about 2026 being an acceleration year. I was overjoyed. The thesis was complete. Now all I had to do was to sit back and enjoy it.

Then the CFO Jamie Miller started talking, in her monotone, dreary way, and I felt an instant spike of cortisol as I listened to her describe how they were seeing basket sizes decreasing and concerning trends in the macroeconomic environment.

I checked the stock ticker as she was speaking and saw that all momentum was killed instantly and the gains were already being given back. She had single handedly killed the stock rally within seconds. The market was not impressed with what she was saying and beige was I.

I was in denial about the seriousness of her bearishness. Alex Chriss was not aligned with her and looking back this could have been the first signal that trouble was afoot.

Any time he got a question in the Q&A he would try to drag the conversation back to the positives. The Open AI partnership. Venmo. They announced a dividend (another potential warning sign). But it was framed very positively and whilst I was not a fan of the timing, I could see the rationale.

This was Alex’s last chance to flip the narrative. It appears that he almost managed it, and was then hamstrung by his CFO.

Sentiment flipped from mega bullish back to ultra bearish in the space of a few hours and before long the stock was back in the $60s.

I did find it alarming at the time how different in tone and demeanour Jamie was to Alex, but I wrote it off as her having terrible social and communication skills. That, also was a mistake.

That was another signal.

To the trained eye, issues were present. I spotted them but I chose not to act.

I was still excited about the Open AI partnership and other things in the pipeline.

I thought the dividend would drive value investor inflows into the stock.

With an ever decreasing share count and high institutional ownership, I was perceiving a potential demand and supply issue which could drive stock momentum going forward.

The Fireside Chats

December 3rd 2025. A date I will not be forgetting anytime soon. Jamie Miller was speaking at the UBS global technology conference.

Naively, I thought she may have reflected and learned from her mistakes during the Q3 earnings call.

As I listened to her I felt a sense of impending doom. She was essentially trashing the company.

Multiple references to macro issues and consumer stress.

Warnings about branded checkout slowing down. “At least 2%” slower than the previous quarter. Not good.

She did though, state when asked that guidance was not a problem. This was 2 months before Q4 earnings. So I am not sure how she could say that in good conscience. But there you have it.

I was left deflated after listening to the conference. I posted about this on X and even sold out of the stock briefly.

I knew Wall St would downgrade to oblivion. And who could blame them after listening to that car crash.

My first instinct was the right one.

I am skilled at spotting red flags and my internal alarm was sounding.

Internal Battle

When the stock returned to the $50s I started considering a re-entry. I had upset the PayPal bulls. As one of the most prominent commentators of PayPal, I felt an obligation to the stock and the community I had built. This was yet another mistake. It was not my responsibility. And it clouded my judgment.

The reaction of other bulls I respected at the time were an influence on my decision making too. They could not understand why I sold out. I started to doubt myself. Had I just sold the bottom out of frustration?

Was I over reacting? The stock was still cheap. We still had Q4 and 2026 guidance approaching in a couple of months.

In the late $50s, I started to convince myself the risk vs reward was back in a favourable profile. And I started scaling back in, ending up with a cost basis of $58.

My fate was sealed. I would hold until Q4 and then I would reassess.

This was a mistake. And the only person to blame for it is myself. Not the PayPal bulls who were appalled by my decision to sell out. But me, for allowing their words to influence me in any way. It was not the only factor in my decision making, far from It, but it was a factor.

Losing face was also a factor. I had been vocal about PayPal being the most misunderstood stock in the market. I was not yet ready to accept defeat. And that, broke one of my fundamental rules. Which is not to allow pride or ego to influence investing decisions.

The bull thesis still made sense before Q4 on paper. Jamie was clear on the fireside that guidance, at least would be achieved.

Q4 is usually the companies best performing season. Braintree would be fully contributing by this point and could generate a surprise in revenue growth.

I was keen to see 2026 guidance. Were they sandbagging again? Would revenue re-accelerate and shock the market?

I genuinely did still think that was possible.

It was a reasonable assumption to think Q4 would come in strong. In fact, I assumed it would. I was not even concerned about the results.

I was however, concerned about 2026 guidance. That was the wild card in my head and I knew the market would care about that more than the quarterly results.

There were quite a few things I was not happy with, I was vocal about that publicly. And I had already made a plan to reassess with a view to selling out after Q4 earnings if I did not see what I wanted to see.

The Market Environment

The stars had aligned for a disaster. As was becoming an all too familiar theme for PayPal, they seemed to report during unfavourable market conditions. This time was much worse. The market was already in a bad mood. It was selling off stocks on good earnings. It was punishing poor earnings brutally.

Fintech had had a terrible year too, which no doubt was a factor in some of $PYPL price action.

I was getting uncomfortable leading up to Q4. I had a bad feeling which I could not shake. This was my intuition telling me to de-risk here. An instinct which I again chose to ignore at my own peril.

I was oversized. When I bought back in, it was a small position but the perception of a cheap valuation tempted me to buy way more than I should have. This was yet another mistake and one would pay for dearly.

I was however, anticipating a triple beat and a potential raise despite Jamie’s bearish commentary, and some not so great commentary from Alex too.

With how oversold the stock was and how cheap it had become. It made sense to at least see the facts before making a decision.

I thought a modest uptick or at worst slightly down to flat were the most likely outcomes. I would make my decision and sell regardless of price movement.

The Car Crash

The morning of Q4 came and I had barely slept the night before. Another sign that I was doing the wrong thing. You really are your own worst enemy when it comes to the stock market. This was a prime example. If I truly believed in my rationale then I should not have felt this uncomfortable.

I went out for a walk with my wife prior to the numbers being announced. This was intentional as I had been staring at my phone all morning. I left my phone at home.

When I returned, I logged into my brokerage to see the stock tanking and I knew some sort of rug pull must have taken place.

I saw that Alex Chriss was being removed and I knew it was game over. I quickly checked the results, saw that they were bad and then I sold the stock without hesitation at $46. A -20% loss and a total portfolio value loss of -10%.

I felt sick. 2027 guidance removed.

Branded checkout growing at a pathetic 1%. FCF weaker than expected. The CEO jettisoned without warnings simultaneously with an awful quarter and poor 2026 guidance.

A rug pull of the highest order.

I felt betrayed. I felt lied to. Management had been the opposite of transparent here despite claiming to be so.

And the new CEO was going to be the 5 year sitting chairman of the BOD who was present in the Shculman days? No thanks

I was done. I am done. I do not invest in companies who can’t be trusted. And it was clear to me this BOD was no longer worth my time.

The future of PayPal

I am not naive enough to assume that PayPal will not ever rise again.

It may. The new CEO may do a good job of cutting costs and reducing the bloated headcount.

But I do think there is a deep rooted culture problem at the company. It is marred with corporate bloat, ineffective execution and unacceptable delays in all aspects of its business.

In Q4 we still did not hear anything about PayPal Ads. We got zero updates on PayPal World, FastLane, or any other innovations announced and not followed up.

PayPal has been a PR engine without the execution and it’s really shown in these horrific results.

Yes, this may be the kitchen sink quarter to pave the way for the new CEO to outperform.

His compensation package is more orientated on incentives for price appreciation.

He may succeed. PayPal may be a $300 stock again one day. Who knows. If they can maintain their FCF and avoid negative growth, they can realistically buyback all of their shares within a few years. Anything can happen.

But they are still guiding for negative EPS growth despite being able to savage their own share count to juice EPS.

They still have not accelerated buybacks.

They have still withdrawn 2027 guidance.

They have still been completely reckless with shareholders money since 2021.

And the man who oversaw the board throughout that whole period will now be in charge.

I don’t know about you, but that situation is not for me, no matter how cheap the stock has become.

Final thoughts

It’s been a rough year for me so far. I am extremely self critical so the self loathing was strong for a good week or two. I could not bring myself to put pen to paper until now.

Alas, my embarrassment is no reason to keep the cold hard truth from my readers.

If you can learn something from my experiences here then this is not a waste of time.

I will never make these same mistakes ever again. Never again will I ignore my gut or overlook red flags just because I want a thesis to work.

Never again will I put pride above reality. Never again will I ignore what my intuition is screaming in my face.

The knowledge I have acquired from this bitter journey is worth far more than the money I have lost.

I will be stronger for this. I will be better.

Less likely to choose hubris over humility.

More likely to see the reality and act on it much faster from now on.

I hope you can extract some value from these ramblings.

My writing is not structured. I sit over the space of a few hours and I pour out my thoughts.

If you find my work useful, consider sharing so that others can benefit too.

Disclaimers

I am not a financial advisor and this isn’t financial advice.

I have never told anyone to buy or sell a stock, nor would I.

That is an individual decision based on one’s own due diligence, research and thought processes.

I no longer hold a position in PayPal and accept my associated bias.

I take no responsibility for anyone who has acted based on my content.

My content is for educations purposes only.

Nice article! Feels like a bit of a diary entry as well.

Help you get rid of your emotions haha.

Also, no need to be so self-critical. Just be reflective without paining yourself too much.

You’re smart, keeping it real and willing to learn.

A recipe for success

Wait and see what happens